Here is the corrected and divided text: So what actually qualifies you as a sole proprietor, okay, a unique, self-directed 401K, or any of these other fancy phrases? Well, first off, there is no such thing inside the tax code. The tax code just defines what is a 401K, that's it. In a story, the Pension Protection Act came out that said, "Hey, for certain types of 401K plans, and thus this self-directed 401K marketing stuff, for certain types of retirement plans, you don't even need to file a tax return unless the assets of the plan are over $250,000." So, if your self-directed 401K has assets of $199,000, no big deal. You don't need to file a retirement plan in most situations. So, what were the qualifications that came out in the Pension Protection Act? First off, you cannot have any common law employees and get the preferential tax reporting or lack of tax reporting. Next, the plan can only cover the owner of the business and/or their spouse in most cases. So, if I'm a sole proprietorship, it can only cover myself and my spouse. If I'm in a partnership, the plan can only cover those people who are partners of the partnership. If the partnership has any employees who are not owners of the partnership, then you don't qualify for these new reporting requirements under the Pension Protection Act. Let's talk about a corporation. The only people who can be involved in the retirement plan are those people who are 2 percent or greater owners of an S corporation. So, in the context of S corporations, so long as the only participants in the retirement plan own greater than 2 percent of that S corporation, you still qualify for that lower level of tax reporting. And then finally, for C...

Award-winning PDF software

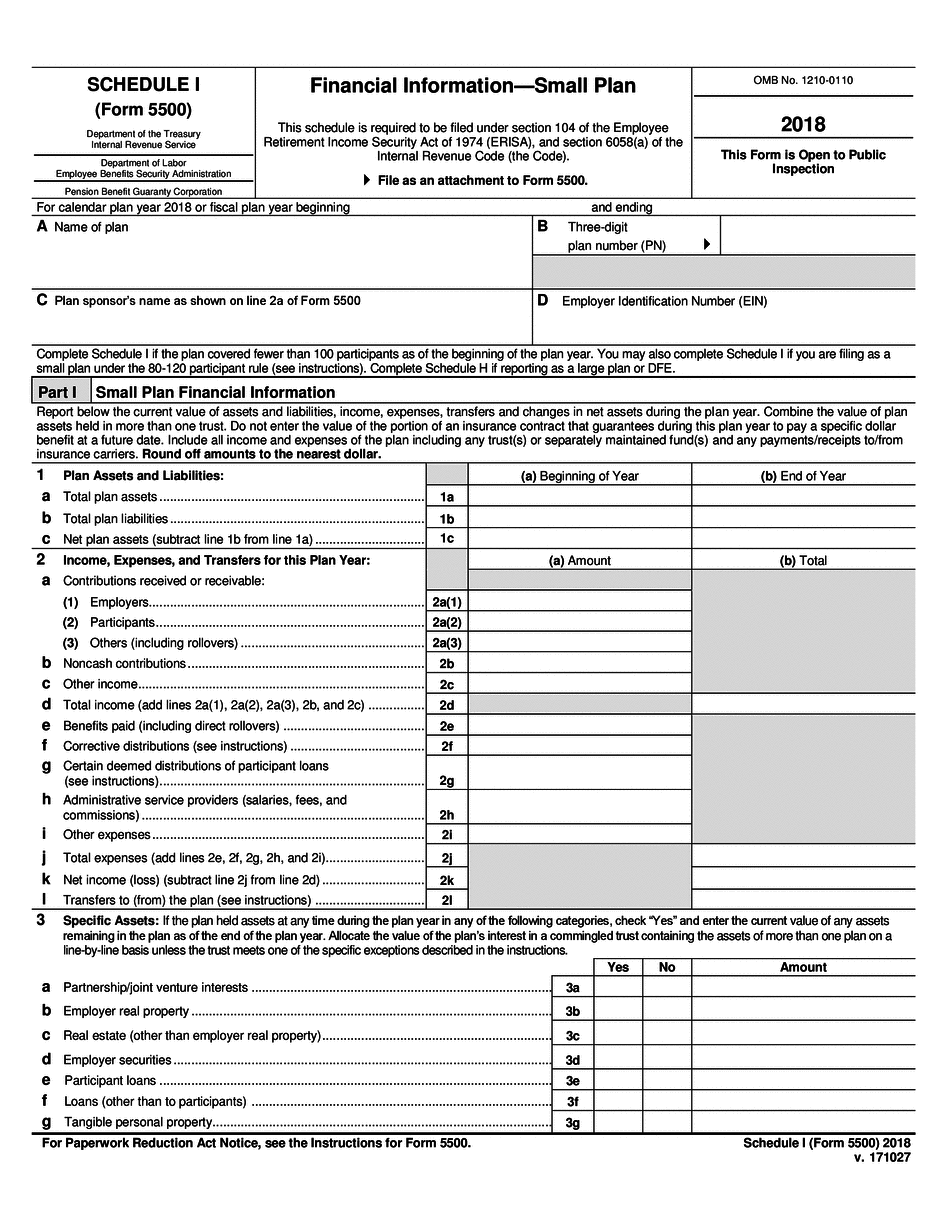

Who needs 5500 - Schedule I Form: What You Should Know

If the Form 5500 is received after that date, the employer is not required to file it. The Forms 8809 and 8805 are also required, so all plan sponsors and their employees should have to file them. If you don't do it by the 10th month prior to the plan year date, there is no penalty; failure to file the Form 5500 by the 13th month of the plan year is a violation of IRS law, but not criminal. Who is subject to filing Form 5500? — SHAM What is the Form 8809: Employee Benefits Security Administration Form 8809: Form for Employer-Sponsored Pension Plans — Business Forms Employees who are participants in qualified pension plans and are covered by ERICA should file the Form 8809. If your plan is not ERICA covered, you are not required to file the Form 8809, but you need to file if it qualifies as an ERICS-covered plan. The purpose of the requirement for filing an 8809 is to show the plan status of qualified plans and ERIC plans that are subject to IRS Form 5500. The 8809 is to be filed within 60 calendar days of the plan year in which they become effective. What to include in the Form 8809 — SHAM Do not file the Form 8809: — If you have already filed an ERICA filing. If so, do not file Form 8809. If you have not filed an ERICA filing, the 8809 will be completed on a separate Schedule MB and Schedule SB. See Section 3 of the FAQ for more information. — If you plan to offer deferred compensation. The Form 8809 and Form 9609 are generally filed at the same time as the Forms 5500 and 5500-EZ. The Form 9609 must be filed by the 12th month of the following tax year. What happens to Form 8509 if you do not file? What happens to Form 8509 if you do not file? Form 8509 is filed if the plan sponsor had 100 or more participating employees that were enrolled in either or both of the plans on Dec 31, 2012. The 8509 is due no later than the 15th month following the plan year date. There is no penalty if you do not file. The following instructions are for Forms 8509 and 8509-EZ only.

Online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 5500 - Schedule I, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 5500 - Schedule I online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 5500 - Schedule I by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 5500 - Schedule I from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Who needs Form 5500 - Schedule I